Insurance Restoration: Process, Timeline & Documentation

Insurance restoration refers to the process of repairing, rebuilding, or restoring a property after a covered loss to return it to its pre-loss condition. It translates policy decisions into real-world repairs.

This phase of the claims process is inherently complex. Multiple stakeholders—homeowners, adjusters, agents, and restoration contractors—must coordinate under pressure, often while the property is unusable or even unsafe.

This guide walks through the typical insurance restoration process, including key requirements, coverage considerations, and practical recommendations for how stakeholders can coordinate effectively to achieve harmonious outcomes.

What is included in insurance restoration

Insurance restoration typically covers repairs required to address accidental damage caused by covered events. While coverage varies by policy and carrier, it often includes:

Water damage from burst pipes, appliance failures, or roof leaks

Fire and smoke damage, including structural repairs and remediation

Mold remediation, often limited in scope and subject to policy caps

Emergency mitigation services, such as water extraction, drying, boarding, or tarping

Deductibles, coverage limits, and exclusions usually apply, and directly affect what is approved for restoration. For example, flood damage, long-term moisture issues, wear and tear, and delayed maintenance are generally not included in standard homeowners’ insurance policies and require separate insurance.

The complexity of restoration coverage can sometimes make it difficult for homeowners to understand what is covered—and why—especially during an already stressful event. For this reason, capturing the full scope of loss before restoration begins is essential to ensure insurers determine and outline coverage clearly, reducing disputes later in the process.

Increasingly, insurers and restoration professionals are turning to comprehensive digital documentation methods—such as 3D digital twins—to create an objective record of property conditions. When pre-loss or baseline property data is available in this format, all stakeholders can align more quickly on coverage decisions, repair scope, and next steps.

The typical insurance restoration process and timeline

Insurance restoration involves multiple stakeholders working together to return a property to its pre-loss condition. Key participants in this process include:

Homeowners, who report and oversee the claim

Insurance adjusters, who assess the damage and confirm coverage

Agents, who facilitate communication between the insurer and policyholder

Restoration contractors, who execute repairs

This section examines the standard steps in the insurance restoration process. It explains what each stakeholder does at every stage, typical timelines, and tips for effective coordination.

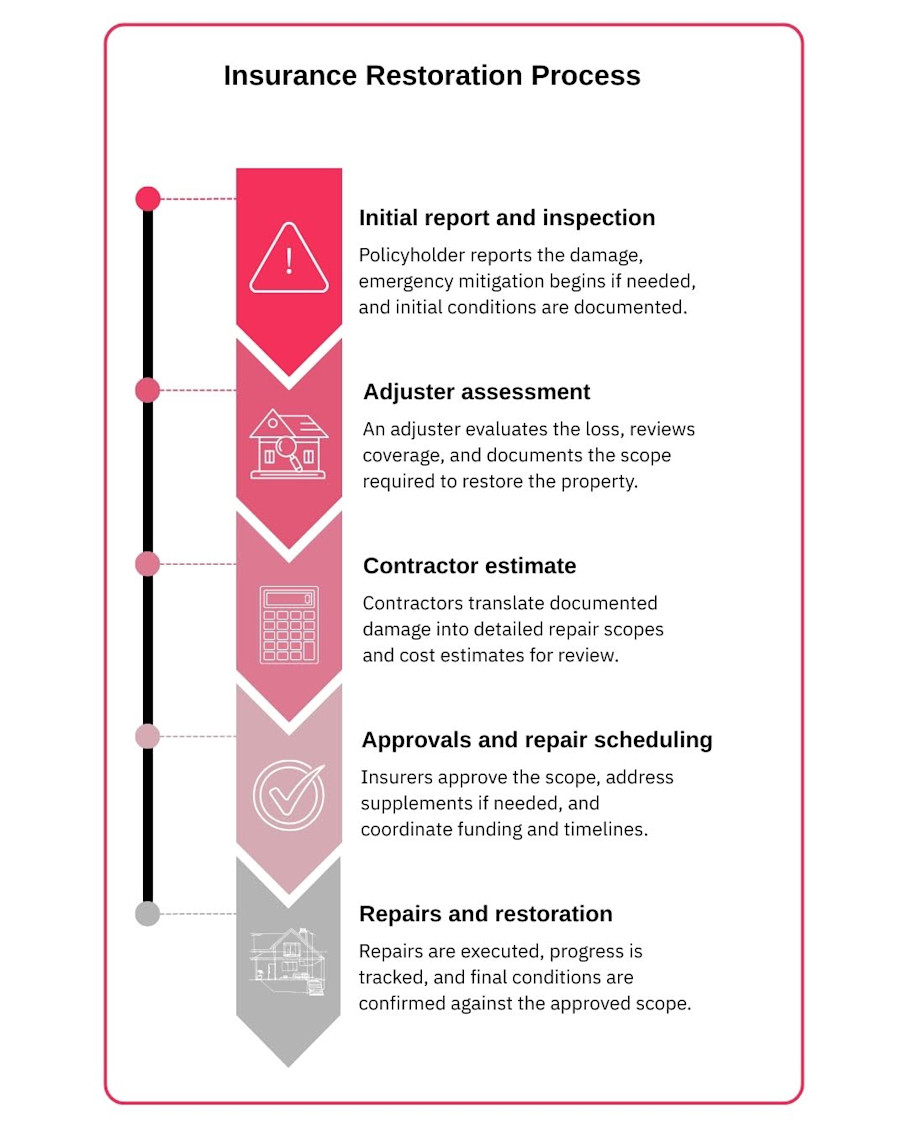

1. Initial report and inspection

The process begins when a homeowner reports a loss to their insurance carrier. After the claim is submitted, the insurer typically schedules an initial inspection to assess the damage and determine immediate next steps. Emergency mitigation—such as water extraction, tarping, or securing unsafe areas—often takes priority to prevent further damage.

Timelines from event to inspection can vary, but prompt reporting is critical to ensure coverage and minimize ongoing losses. Here are estimates for timelines based on some specific loss scenarios:

Scenario | Timeframe | Notes |

Urgent individual losses (e.g., burst pipe, fire, small-scale water intrusion) | Within 24–48 hours of reporting | Inspections are usually scheduled quickly to enable immediate mitigation and prevent further damage. |

Standard claims (moderate damage to a single property) | 3–7 days | Allows time for adjuster scheduling, contractor availability, and initial documentation. |

Large-scale or area-wide disasters (e.g., hurricanes, floods affecting multiple properties) | 1–2 weeks or more | Response times can be extended due to high claim volume and limited adjuster availability; emergency mitigation may still occur first. |

Capturing the property’s pre-restoration condition during this phase is essential: it establishes a clear baseline for the claim, supports accurate coverage decisions, and helps prevent disputes later.

Comprehensive digital property records, such as 3D insurance scans, provide a detailed, verifiable snapshot of the property. These records reduce the need for multiple in-person visits and create an objective reference for adjusters, contractors, and homeowners throughout the claim.

2. Adjuster assessment and documentation

Once the initial inspection is complete, the insurance adjuster reviews the damage, evaluates coverage, and begins documenting the scope of repairs.

Adjusters often juggle multiple claims simultaneously, coordinating with homeowners and contractors while managing tight deadlines. Here are some common timeline ranges for the assessment and documentation stage:

Scenario | Timeframe | Notes |

Minor or straightforward claims | 1–3 days | Quick assessments are possible when damage is limited, documentation is clear, and coverage questions are minimal. |

Moderate claims | 3–7 days | Involves more detailed documentation, measurements, and coordination with contractors; may include verification of emergency mitigation. |

Complex or large-scale claims | 1–2 weeks or more | Multiple rooms, structural damage, or area-wide events require careful documentation and possibly multiple site visits; high claim volume can extend timelines. |

Traditional documentation methods—manual measurements, photo logs, and paper forms—can be time-consuming and prone to errors.

Alternatively, many adjusters are modernizing the claims process by using digital tools. Digital twins generate standardized property reports, measurements, and schematic floor plans automatically. Cloud-based sharing of these records allows adjusters to inspect properties remotely, confirm details without repeat site visits, and provide standardized field documentation to all stakeholders. This helps ensure decisions are based on verifiable, shared information and cuts claims cycle time.

3. Contractor scope and estimate

Restoration contractors use the adjuster’s documentation to create detailed repair scopes and cost estimates. Accuracy at this stage is critical: overlooked damage or misinterpreted measurements can lead to disputes, delayed repairs, and costly change order management.

Again, timelines vary based on the scope of the restoration:

Scenario | Timeframe | Notes |

Small, straightforward repairs | 1–2 days | Quick scoping and estimation are possible when the damage is limited and documentation is clear. |

Moderate repairs | 3–5 days | May involve multiple rooms, specialized trades, or coordination with adjusters to verify coverage details. |

Complex or large-scale losses | 1–2 weeks | Large-scale or multi-family property insurance estimations require detailed measurements, multiple contractors, and coordination with adjusters or engineers. High claim volumes can extend timelines further. |

A complete, visual record of the property from a digital twin allows contractors to identify all areas that require attention and supports faster, more reliable estimates. When estimates are based on shared, standardized property data, all parties work from the same information, reducing errors and misunderstandings.

Digital property records can be converted into estimation-ready formats for faster line-item calculation and integration with industry-standard tools. Matterport also provides instant, estimation-ready 3D Sketch (SKX) files. Sketch for Cotality Estimate and TruePlan for Xactimate can be integrated with industry-standard tools for faster line-item calculation.

These loss sketches are dramatically faster than manual services that typically take hours or days. They are automatically generated in just minutes and include automated, annotated dimensions that help adjusters, restoration contractors, and CAT teams move from inspection to estimate to claims approval much faster.

4. Approvals and repair scheduling

After estimates are submitted, insurers review the scope, verify coverage, and release funds for restoration. This stage ensures that the planned repairs align with policy terms and that all parties agree on the scope before work begins.

Timelines for approvals depend on the complexity of the loss:

Scenario | Timeframe | Notes |

Simple claims (limited damage, single estimate) | 1–2 days | Approvals are usually quick when documentation is clear and coverage questions are minimal. |

Moderate claims (multiple rooms, trades, or supplemental requests) | 3–7 days | Review may involve clarifying line items, coordinating with contractors, or validating additional costs. |

Complex or large-scale losses (multi-property, structural issues, high claim volume) | 1–3 weeks or more | Complex claims often require multiple rounds of review. |

Delays are common at this stage and can occur due to a number of factors, such as:

Multiple estimates: When different contractors or trades provide overlapping or conflicting scopes, insurers may need additional time to reconcile the differences and approve a unified plan.

Supplement requests: Unexpected damage discovered during initial mitigation or demolition often requires additional estimates or adjustments to the original scope, which must be reviewed and approved.

Seasonal backlogs: During peak seasons—such as hurricane, winter storm, or wildfire periods—high claim volumes can create scheduling bottlenecks for adjusters and contractors.

Material shortages: Delays in obtaining construction materials or specialized equipment can affect both the timing of approvals and the scheduling of restoration work.

Efficient insurance document management at this stage helps accelerate approvals and minimizes the risk of re-inspections or disputes. Shared digital property records can act as a single source of truth, allowing adjusters and insurers to confirm scope remotely, align on any changes, and reduce repeated site visits—especially for large or complex claims.

5. Repairs and restoration

The final phase of insurance restoration covers demolition, mitigation, rebuilding, and final inspections. Timelines for this stage depend heavily on the severity of the damage and the scope of repairs. For example, minor water damage confined to a few areas (such as a kitchen or bathroom) may resolve in a matter of weeks, whereas major structural reconstruction—especially in larger homes or multi‑unit properties—can stretch into many months.

Factors that impact the duration of the restoration project include:

Severity of damage: More extensive structural compromise (e.g., framing, roofing, or foundational issues) requires more demolition, engineering, and phased work.

Scope of repairs: Renovations that span multiple trades (plumbing, electrical, HVAC, roofing, carpentry) take longer to schedule and complete.

Permitting and inspections: Rebuild work often triggers local building permits and inspections, which add time between phases and before final occupancy.

Resource availability: Labor availability, subcontractor scheduling, and material lead times (especially for specialty items) can extend schedules, particularly during peak seasons or widespread disaster recovery.

Here are some broad timelines based on the scope of the actual restoration work:

Scenario | Estimated Duration | Notes |

Localized / Minor repairs | 2–4 weeks | Repairing one or two rooms, painting, drywall patches, and minor finish work. |

Moderate repairs | 6–12 weeks | Multiple rooms or partial structural repair, systems (plumbing, electrical) alignment, and coordination of trades. |

Major restoration | 3–6+ months | Whole‑house repair or reconstruction, extensive structural work, code compliance upgrades, and permit‑dependent tasks. |

As repairs progress, maintaining synchronization between the approved scope and the work being executed is critical. Periodic digital captures of a property can be overlaid against each other to confirm the project is aligned from one phase to the next.

The Matterport and SIMLAB STAGES integration allows restoration contractors to compare rough‑construction models to both the approved work and the finished conditions that were agreed upon. This ensures continuity at each milestone.

Common friction points in insurance restoration (and how to solve them)

Insurance restoration involves multiple stakeholders coordinating under stressful circumstances, often while properties are partially unusable or unsafe. This complexity, combined with sensitive work and high expectations, can create friction at multiple points in the process.

Clear, accurate documentation can help mitigate many of the most common challenges:

Misaligned expectations: Homeowners, contractors, and adjusters may interpret damage or repair scope differently. Accurate 3D documentation captures the full extent of damage, tracks mitigation progress, and supports defensible, objective estimates. In an ideal scenario, pre-loss documentation should be captured during policy creation to provide a reference of the former property condition for accurate scoping.

Delays in approvals: Insurers and contractors may need to clarify or reconcile work scopes and construction cost estimates. Thorough documentation helps align restoration contractors and insurers efficiently, reducing back-and-forth and speeding up approvals.

Subcontractor coordination: Multiple trades must schedule work in a specific order. Remote construction collaboration tools allow contractors to align on scope virtually, reducing scheduling conflicts and ensuring teams know what to tackle at each stage.

Unexpected conditions: Damage can be more extensive than initially documented or hidden issues may emerge during mitigation. Virtual walkthroughs allow contractors to inspect conditions ahead of time and adjust plans proactively.

Communication gaps: Instructions, approvals, or progress updates can be lost across emails, calls, or paper notes. Tags and Notes in digital twins provide context for approvals, special instructions, or mitigation steps, streamlining communication and giving insurance professionals a clear reference.

Verifying completion: Stakeholders may disagree on whether repairs meet approved scope or quality standards. Digital twins and overlays support defensible documentation of completion, giving confidence that restoration meets the approved specifications.

A shared, verifiable record—from pre-loss condition to final completion—creates transparency to help restore properties efficiently and fairly.

5 documentation best practices for faster and fairer insurance restoration

Matterport’s 3D digital twins provide a single, objective source of truth throughout the restoration lifecycle. To translate these tools into real-world results, keep these five best practices in mind at every stage of the restoration process:

1. Capture at every stage: Document the pre-loss condition, extent of damage, mitigation progress, and completion verification. Early captures reduce ambiguity and provide a reliable baseline for every decision.

2. Create defensible documentation: Records should be clear, complete, date-tied, room-by-room, measurable, and easy to audit. This ensures that any future review—by insurers, contractors, or even in legal contexts—is straightforward and credible.

3. Document these minimum requirements at each stage:

Pre-loss / baseline: Full property scans, critical systems, and structural features.

Damage assessment: Photos, measurements, and notes for all affected areas.

Restoration progress: Evidence of temporary repairs, drying, or structural stabilization.

Completion: Verification that work matches the approved scope and finishes are consistent with plans.

4. Provide a supported repairs estimate: Include sketches, accurate measurements, material quantities, equipment logs, labor assumptions, and line-item rationale. This creates transparency for insurers and contractors, making approval and reconciliation faster.

5. Prevent disputes proactively: Compare the property before and after disaster restoration using consistent documentation and shared digital property records to reduce misalignment, communication gaps, and unexpected surprises that can slow approvals or trigger supplemental claims.

Property damage events are chaotic, and aligning homeowners, adjusters, and contractors has historically been a fraught process.

Today, 3D digital twins have reshaped the restoration process. By making restoration claims more efficient, accurate, and transparent, they turn a traditionally fragmented, stressful process into one that stakeholders can navigate confidently—restoring not just properties, but clarity and trust.

Get in touch with our team