Home Contents Insurance Guide: How To Use Digital Twins For Effective Property Documentation

Home Contents Insurance & Property Inventory Guide

While property owners, tenants, and business owners are often well-acquainted with property or renters insurance, not as many are familiar with another crucial type: home contents insurance.

In the case of a catastrophic event like a fire or a robbery, you’ll want protection for more than just the four walls of your property—you’ll need coverage for your possessions inside those four walls. And that’s where insurance for the contents of homes comes in.

Below, you’ll learn the ins and outs of home contents insurance, what you’ll need to get a policy, and its many advantages.

What is home contents insurance?

Home contents insurance, which is synonymous with “personal property insurance” or “contents insurance,” is a form of personal property insurance that covers your belongings in your house in case of accidental damage. Basically, this home contents insurance will help you financially recover in the case of a fire, flood, theft, or other event destroying your personal items.

Obtaining a home contents insurance policy is a wise move whether you rent or own your property. Either way, the contents of your home will be protected against unexpected loss. Your home insurance policy or condo insurance policy may include clauses with personal property coverage, but it’s always a good idea to double-check.

To get coverage, you’ll need to provide your insurer with a detailed inventory of your belongings. But what should you include? Listing every single belonging in your house is an overwhelming task in itself.

Possessions to include in your home inventory

Rather than cluttering your home inventory list with low-cost, easy-to-replace items (like your sets of sheets for the guest room), focus on high-value items like:

Jewelry

Artwork

Musical instruments

Pricey hobby equipment (like that vintage film camera)

Collectibles (like that impressive coin collection)

Furniture

Electronics

Home appliances

Pricey lawn care equipment (your riding mower, tractor, weed whacker, etc.)

Big-ticket, expensive items in a storage locker or facility (yes, a home contents insurance policy covers your off-site belongings as well)

What info to include in your home contents inventory

When walking around your home documenting all your belongings, you’ll need to capture specific pieces of info to hand over to your home contents insurance provider.

You can certainly add all these details into a spreadsheet—like this home inventory template for Excel—or you can use technology to combine photo and written documentation of your inventory.

Whatever method you choose, ensure you list this info for each of your belongings:

Basic details

- A quick description of each item

- Where you bought it

- Make and model

- How much you paid for it (actual cash value)

Serial numbers for home appliances and electronics

Proof of value (any receipts, appraisals, invoices, or certificates)

Photos (add these with your description of your items)

4 benefits of maintaining household inventory for home contents insurance

Making and maintaining an inventory for your home contents insurance is a crucial part of obtaining a policy. But this process also offers a wealth of other advantages. Just a few of the top benefits include:

1. Documentation and organization

When you create a home inventory, you create a comprehensive archive of all your possessions. You’ll have all the makes, models, serial numbers, and descriptions of your belongings in one central record, like in a spreadsheet or a dedicated app.

That way, in the case of a theft or disaster, you can refer back to this record of possessions to ensure your insurer reimburses you for any covered losses.

2. Accurate valuation

Part of documenting your personal belongings is to provide your insurer with proof of value. Especially for electronics, appliances, and other big-ticket items, keep your receipts or appraisals to demonstrate how much you paid so your policy carrier knows the replacement cost.

Keeping an up-to-date home inventory can make it easier for your insurer to offer the right replacement cost coverage options for your possessions. And, if something happens, it’ll be easier for you to get a payout for the right amount when making a claim.

3. Claims efficiency

An updated home inventory can make submitting an insurance claim less of a headache. When you’re struck by a disaster, you won’t need to add to your stress by trying to rack your brain for details of the possessions destroyed or stolen in your home.

Instead, you’ll have a comprehensive list of your belongings you can refer to and send to your insurer with your claim. Having accurate information on hand can speed up the claims process and ensure your insurer pays out the appropriate value for your belongings.

4. Facilitating policy review and updates

When you regularly update your home inventory, it’s easier to ensure you have the appropriate home contents insurance coverage. We recommend you review at least once a year and add new purchases, updates to valuations, and other relevant info.

During this review process, check in on your current home contents policy. Do you still have appropriate protection for all your belongings? And does your policy have any exclusions? For example, if you add jewelry, pricey artwork, or furs to your inventory, you may need to explore buying additional coverage—dubbed an endorsement rider or floater—to your policy.

How Matterport transforms the way you document home contents for the better

Documenting your home inventory and passing information to your home contents insurance provider can be time-consuming and challenging. On the flip side, insurance adjusters can spend endless hours sifting through photos and information to process claims.

Fortunately, the right tech and tools can make it easier to collect home inventory info and make the claims process far simpler.

Whether you’re an insurance carrier, claims adjuster, restoration company, or property owner, Matterport’s 3D digital twins and Tags can help create accurate and transparent documentation that leads to fair valuations.

Here’s a quick walkthrough of how Tags work in a Matterport digital twin:

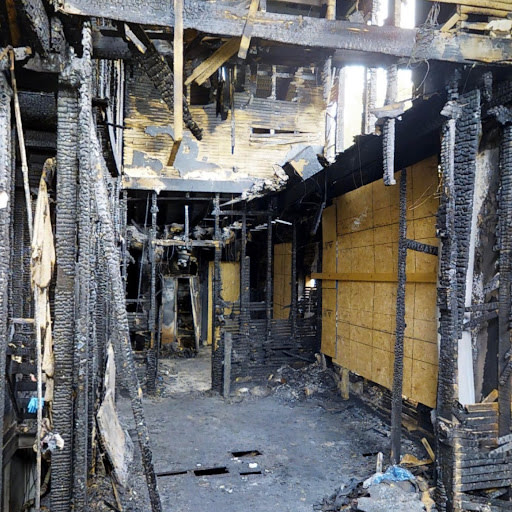

Document pre-mitigation and post-mitigation conditions more accurately

Example of fire-damaged property. Source

Property owners and insurers alike can get the most comprehensive pre-loss asset documentation and risk management with digital twin technology. This allows for more informed and accurate underwriting practices.

With a 3D scan of a property and its contents, property owners can curb the number of policyholder breakage claims with a pre-mitigation scan that captures everything in its current state. This kind of scan can also reduce the initial risk of insuring a building and eliminating the need for physical reinspection. On top of these benefits, it’s simple to add notes right in the 3D model via Tags.

Dry Patrol, a top restoration company in Cincinnati, OH, leans on Matterport’s suite of tools to efficiently work with insurance providers through the estimate and documentation process.

Thanks to 3D documentation, they eliminated many typical questions from insurance companies regarding mitigation strategy, the equipment they used, and pre-existing conditions.

“We use the Matterport camera to document pre-mitigation and post-mitigation conditions with our equipment in place, enabling insurance companies to virtually walk through a property every step of the restoration process,” said Derron Oakley, Partner at Dry Patrol.

“With the Matterport Cloud, we can reference accurate measurements from the models, and auto-generate floor plans to share with insurance companies in Xactimate.”

Provide more efficient insurance estimates

With Matterport, it’s simpler to gather comprehensive documentation for insurance and restoration professionals for estimation purposes. No need to take hundreds of pictures, take measurements, or schedule multiple site visits—you can eliminate all these with a 3D walkthrough.

Rachel Stewart, founder of restoration management software company Xcelerate integrates with Matterport’s digital twins for precisely this purpose.

Her team uses Matterport to scan damaged properties, and an in-house estimator builds out the estimate. From there, it’s easier for Xcelerate to work with the property owner to negotiate with the insurance company.

“We’re able to review estimates after they come back with all of the documentation in one place, and estimates can easily be reviewed side-by-side with the 3D tour,” she said. “Anytime you send an email it automatically connects the 3D tour.”

Because 3D tours have simplified and centralized their estimate process, the team has seen significant time savings. The 3D tours provide an objective way to document and validate claims so insurance companies can make decisions quickly.

“Having everything in one place and being able to get a high-level view has made the claims process so much more efficient and we can close claims faster,” she said. “We probably saved ourselves 40% of our time in the process.”

Accurate claims documentation for home and business owners

Property owners can document homes, businesses, or any assets with the Matterport true-to-life and comprehensive platform, and expedite any potential claims.

With 3D scans, you’ll get a complete record of your property’s condition, plus an accurate home inventory of your belongings. This type of comprehensive documentation can prevent any discrepancies from coming up down the road if you need to make a claim.

Eberl, a firm of adjusters that works with policyholders and insurance carriers, found documenting property damage and losses was a major drag on their time. The team spent endless hours processing, annotating, and labeling photos of impacted sites, followed by more hours of writing reports to validate the damage to structures and interior items.

But Eberl found a better solution: Matterport digital twins. The 3D scans created dimensionally accurate replicas of spaces to better document property loss claims. With the rich visuals and precise measurements, Eberl adjusters were able to quickly and accurately identify property characteristics. This saves tremendous time for both the adjusters and claims processors who need to verify and agree on the report details before claims are approved.

Expedite insurance claims and calculations of property loss

Thorough documentation—like having a 3D scan of your space and Matterport Tags with details of your possessions—speeds up the processing of insurance claims for home contents. With this kind of up-to-date info on hand, you can prevent discrepancies and cut down on processing time often lost to resolving issues.

For example, property owners and adjusters can share links to 3D scans to make it simple to share home inventory info with insurers.

Adjustors can even review a damaged property remotely with a virtual walkthrough (including the space’s exact dimensions)—which can pave the way for a faster claim.

This was exactly the case for Sync Technologies, an Australian firm that synchronizes data to help home builders, restoration companies, and remodeling pros stay on time and on budget. Back in September 2021, Melbourne suffered a 5.9-magnitude earthquake that caused structural damage throughout the region.

Thanks to Matterport 3D scans, adjusters were able to improve response times even when they were spread thin. SyncTech’s insurance customers worked remotely with engineering specialists in New Zealand following the event. The loss adjuster used SyncTech’s digital twins, captured with Matterport cameras, to provide the specialist with everything needed to get the insurance claim processed right away. Some of SyncTech’s customers even scanned their own properties right after they purchased or finished construction, so they can provide “before” and “after” digital twins to their insurance agents.

Still have lingering questions about home contents insurance? Below are some of the most common queries and their answers.